A business valuation is a structured, evidence-based opinion of what your company is worth, produced using one or more of three approaches (income, market, asset) against a defined standard of value, and interpreted against current buyer behavior. Done right, it withstands the IRS, the SBA, opposing counsel, and a sharp-elbowed buyer’s diligence team.

This guide matters because the lower-middle-market valuation conversation is crowded with three kinds of bad inputs: online calculators, broker rules of thumb, and CPA opinions written for tax filings, not transactions. We’ve built this pillar to give owners and their advisors a single reference grounded in NACVA Professional Standards, current Tier 1 market data, and the wedge that confuses most owners: the difference between a Calculation Engagement and a Valuation Engagement.

Duran Advisors serves business owners in New Orleans, the North Shore, Metairie, Baton Rouge, Houma-Thibodaux, and South Mississippi. Every valuation we deliver follows the framework on this page.

By Joel F. Duran, Principal Advisor at Duran Advisors. CM&AA, M&AMI, CM&AP, CEPA, CVGA, Certified Value Builder™, CAIM, CMSBB; IBBA Past Educator; active member of M&A Source, AM&AA, IBBA, and the International Exit Planning Association. 15+ years of M&A and business valuation experience across the Gulf South. Last updated: June 1, 2026.

Key Takeaways

- A business valuation is built around three approaches (income, market, asset) and one standard of value selected to match the engagement’s purpose.

- NACVA distinguishes a Calculation Engagement (Calculated Value) from a Valuation Engagement (Conclusion of Value). The wedge determines court weight, IRS defensibility, and SBA acceptance.

- Per the Exit Planning Institute 2025 Generational State of Owner Readiness, more than 50% of Baby Boomer owners plan to exit within five years, yet only 27% have completed a formal valuation.

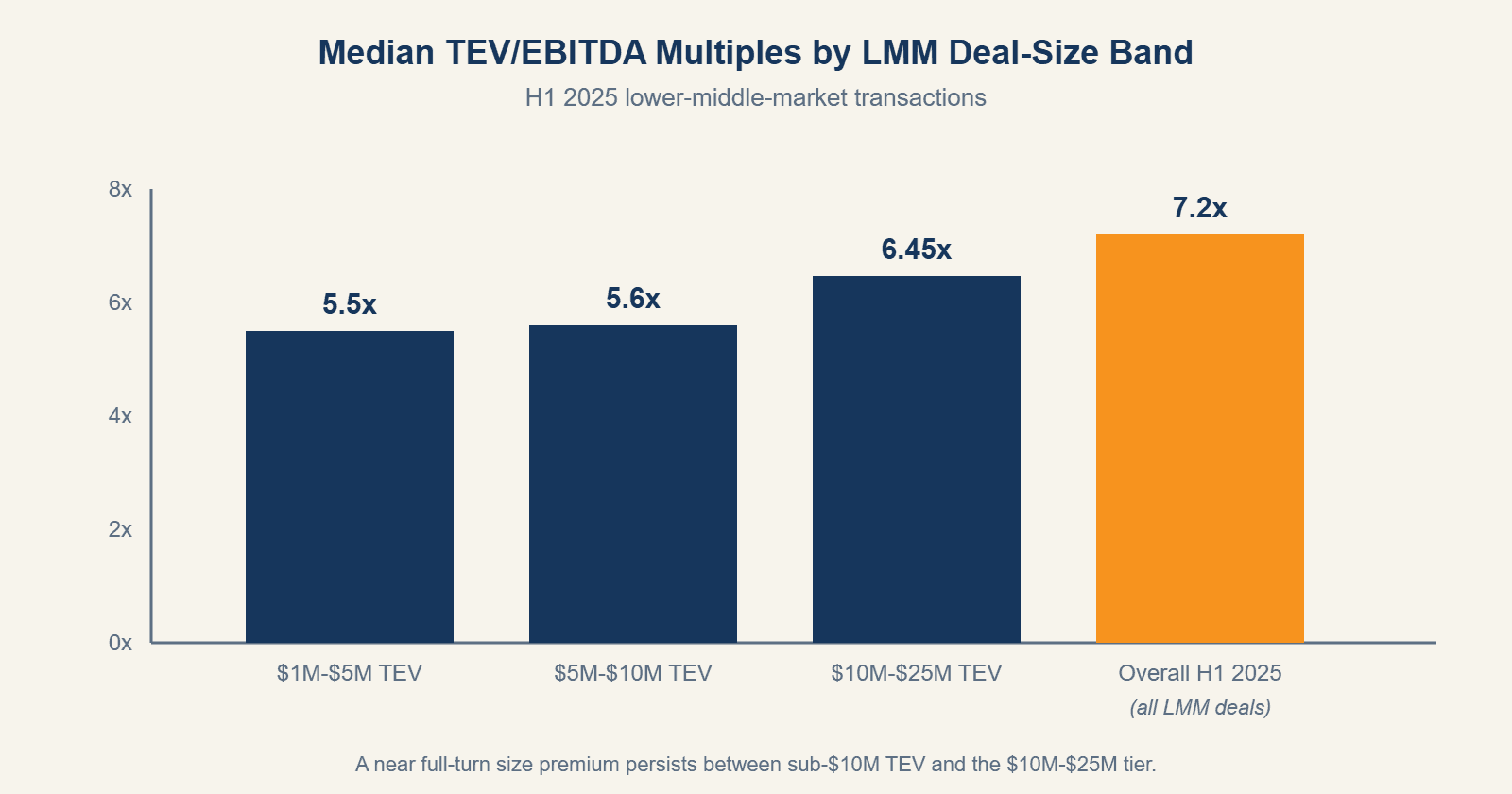

- Lower-middle-market deal multiples in 2025 ran 5.5x EBITDA on $1M-$5M TEV transactions to 6.7x on $10M-$25M deals (GF Data via Middle Market Growth, Fall 2025).

- The valuation you commission before going to market determines how well your deal survives diligence. 44% of dealmakers cite valuation disagreement as the top obstacle to deal closure (KPMG 2025 M&A Deal Market Study).

Why do owners get a business valuation? The six real reasons

Owners commission a business valuation when a decision needs a defensible number behind it. Per the Exit Planning Institute’s 2025 Generational State of Owner Readiness, 50%+ of Baby Boomer owners plan to exit within five years, yet only 27% have completed a formal valuation and only 9% have a documented estate plan. The gap between intent and preparation is where money gets left on the table.

Six engagement triggers come up again and again in our practice. Each one has a specific standard of value attached. Match the standard to the purpose, or the number is wrong before you start.

- Preparing to sell. The pre-market valuation establishes a defensible asking range, exposes the add-backs that buyers will challenge, and surfaces the value drivers worth shoring up before the data room opens.

- Buy-sell agreement funding. Trigger events (death, disability, divorce, departure) collapse the partnership unless the agreement’s valuation formula matches the insurance funding behind it. Independent valuations carry more weight than formula clauses.

- Estate and gift tax planning. Standard of value is Fair Market Value. Revenue Ruling 59-60 lists eight aspects the IRS expects every appraisal to consider, and IRC Section 6662 imposes penalties for tax-valuation misstatements. IRC Section 2703 governs how restrictions on transfer affect value.

- Divorce or partnership dispute. Standard of value varies by state. Federal courts apply the Daubert framework to expert testimony, and the professional-vs-personal goodwill distinction routinely shifts hundreds of thousands of dollars between spouses.

- SBA or bank financing. The 7(a) program requires an independent business valuation when goodwill is being financed. The lender’s standards are non-negotiable.

- Strategic planning and benchmarking. Owners use baseline valuations to set five-year targets and measure progress against value drivers, not just revenue.

The purpose determines the standard of value. Get that wrong and the rest of the report is wasted.

What a business valuation is NOT

A business valuation isn’t a number generated by a website, a multiple your friend’s broker quoted at the country club, or your CPA’s 30-minute opinion. Per the Pepperdine Private Capital Markets Report 2025, guideline transactions carry the largest single weight among valuation methods at 33%, but no single method tells the whole story. Defensibility lives in the reconciliation.

- Not a calculator. Online tools take revenue and an industry code and multiply. They can’t read your customer concentration, your gross-margin trajectory, your succession depth, or how much of the EBITDA is actually owner discretion. For a better do-it-yourself starting point, walk through our 10-minute business-worth self-assessment.

- Not a fixed number. A defensible valuation is a range with reasoning behind it. The reconciliation across the three approaches is the analytical work. The point estimate is the output, not the input.

- Not your CPA in 30 minutes. Tax-return EBITDA isn’t valuation EBITDA. Recasting takes hours, sometimes days, and is where most amateur valuations break down.

The three valuation approaches every credentialed valuator uses

Every defensible business valuation applies one or more of three approaches: income, market, and asset. Per the Pepperdine 2025 Private Capital Markets Report, 76% of practitioners use recast EBITDA multiples as their primary market method, and guideline transactions carry 33% method-weight on average. The reconciliation across approaches is where credentialed work earns its fee.

Asset-based approach

The asset approach builds value from the balance sheet up: tangible assets at fair market value, plus quantifiable intangibles, minus liabilities. It dominates the reconciliation for asset-heavy businesses, holding companies, and liquidation scenarios. For operating businesses with meaningful goodwill, it usually sets the floor, not the conclusion. Book value alone is rarely useful and never sufficient.

Income-based approach

The income approach converts the business’s expected future economic benefits into present value. Three methods do most of the work. Discounted Cash Flow forecasts multi-year cash flows and discounts each year back using a build-up discount rate. Capitalization of Cash Flow, also called the Gordon Growth Model, divides a single-period benefit stream by a capitalization rate. The Excess Earnings Method, codified in Revenue Ruling 68-609 (the Treasury Method), values tangible assets separately from capitalized goodwill.

The identity to remember: Discount Rate minus long-term Growth equals Capitalization Rate. Misapplying that single relationship is the most common error in amateur valuations.

Market-based approach

The market approach compares the subject business to similar businesses that have actually sold. Three methods apply: transactions in the subject’s own stock, the Guideline Public Company Method, and the Merger and Acquisition Method using private-deal databases.

For lower-middle-market deals, the M&A method does the heavy lifting. Per GF Data via Middle Market Growth (Fall 2025), the size premium between sub-$10 million TEV deals and the $10-$25 million tier was nearly a full turn of EBITDA in H1 2025. Per the IBBA Market Pulse Q2 2025, sub-$500K businesses traded at 2.3x SDE while $5M-$50M businesses traded at 5.5x EBITDA. The DealStats Value Index Q1 2025 reported a Q4 2025 median selling price to EBITDA of 3.5x across all industries, which sounds low until you remember it blends every size band and quality tier. The Main Street vs lower-middle-market distinction matters more than most owners realize.

Comp selection is where defensibility lives. Our practitioner rule, the 5/10/10 Principle: never use a transaction newer than the valuation date, eliminate transactions older than five years, eliminate targets ten times bigger than the subject, eliminate targets ten times smaller. That filter alone disqualifies most “comparable” deals in the public databases.

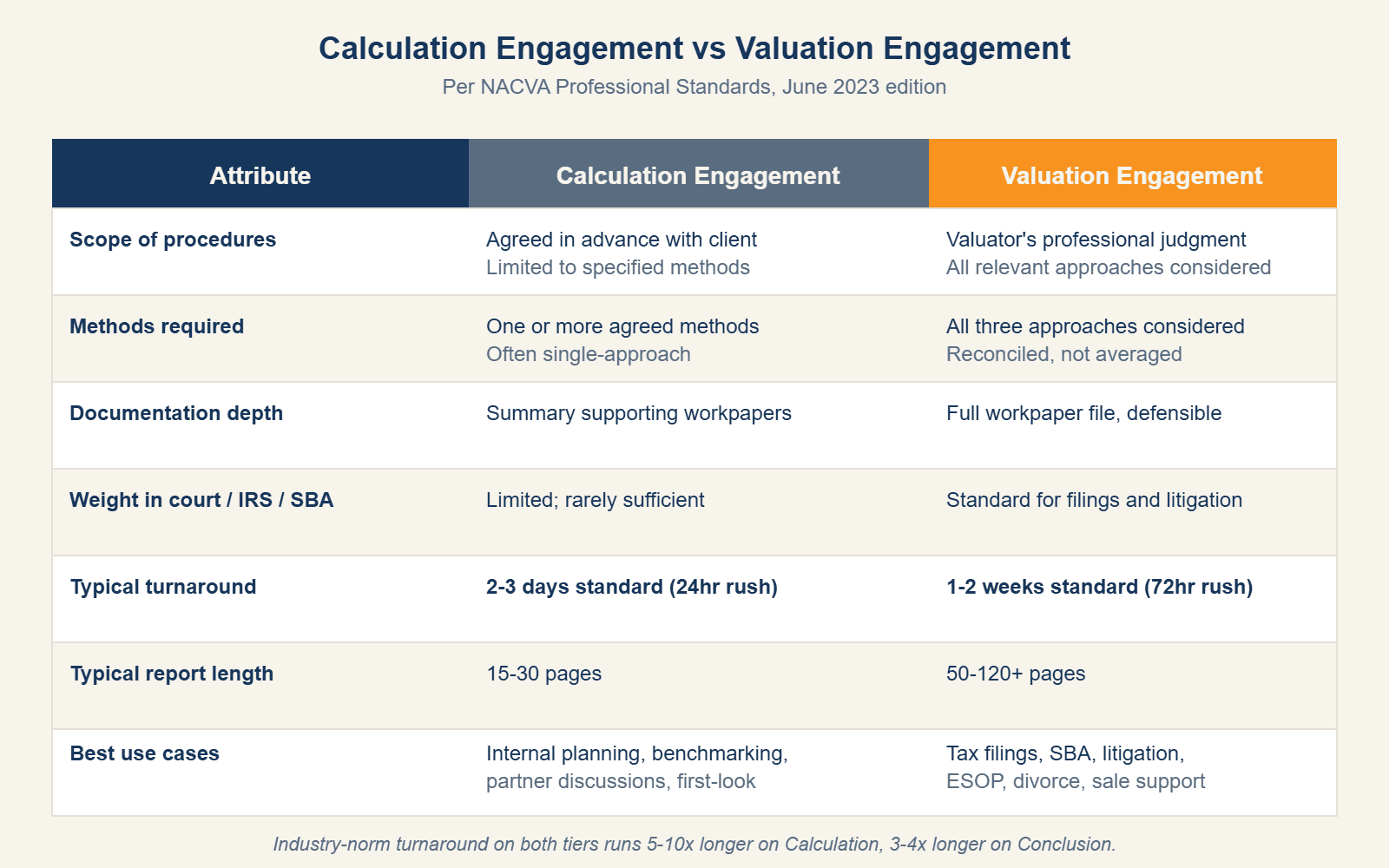

Calculation Engagement vs Valuation Engagement: the NACVA distinction every owner should understand

NACVA’s Professional Standards define two engagement types, and the difference determines court weight, IRS defensibility, and how much the report costs you. Per the NACVA Professional Standards (June 2023 edition), a Calculation Engagement produces a Calculated Value, and a Valuation Engagement produces a Conclusion of Value. Same business, two very different deliverables.

Calculation Engagement (Calculated Value)

In a Calculation Engagement, the client and the valuator agree in advance to specific approaches, methods, and scope. The result is a Calculated Value, often informally called a Calculation of Value. It’s faster, lighter on documentation, and appropriate for internal planning, baseline benchmarking, partner buy-out discussions, or first-look conversations where the owner wants directional clarity without the full audit trail.

Valuation Engagement (Conclusion of Value)

In a Valuation Engagement, the valuator applies whichever approaches and methods their professional judgment deems appropriate, then reconciles them. The result is a Conclusion of Value backed by full documentation. This is the engagement type required for IRS filings, SBA financing involving goodwill, divorce court, shareholder oppression litigation, ESOP transactions, and any context where the report will be challenged by an opposing expert.

Which one do you need? A short decision shortcut.

- Going to be filed with the IRS? Conclusion of Value.

- Going to opposing counsel or a judge? Conclusion of Value.

- Going to an SBA lender for goodwill financing? Conclusion of Value.

- You just want to know directionally where you stand before you start planning? Calculation of Value is usually enough.

One operational note. Our turnaround on a Calculation of Value is 2-3 days standard with a 24-hour rush available, and a Conclusion of Value is 1-2 weeks standard with a 72-hour rush. Industry norm runs roughly 5-10 times longer on Calculation and 3-4 times longer on Conclusion. That speed is structural, not magic: we built the workflow around it.

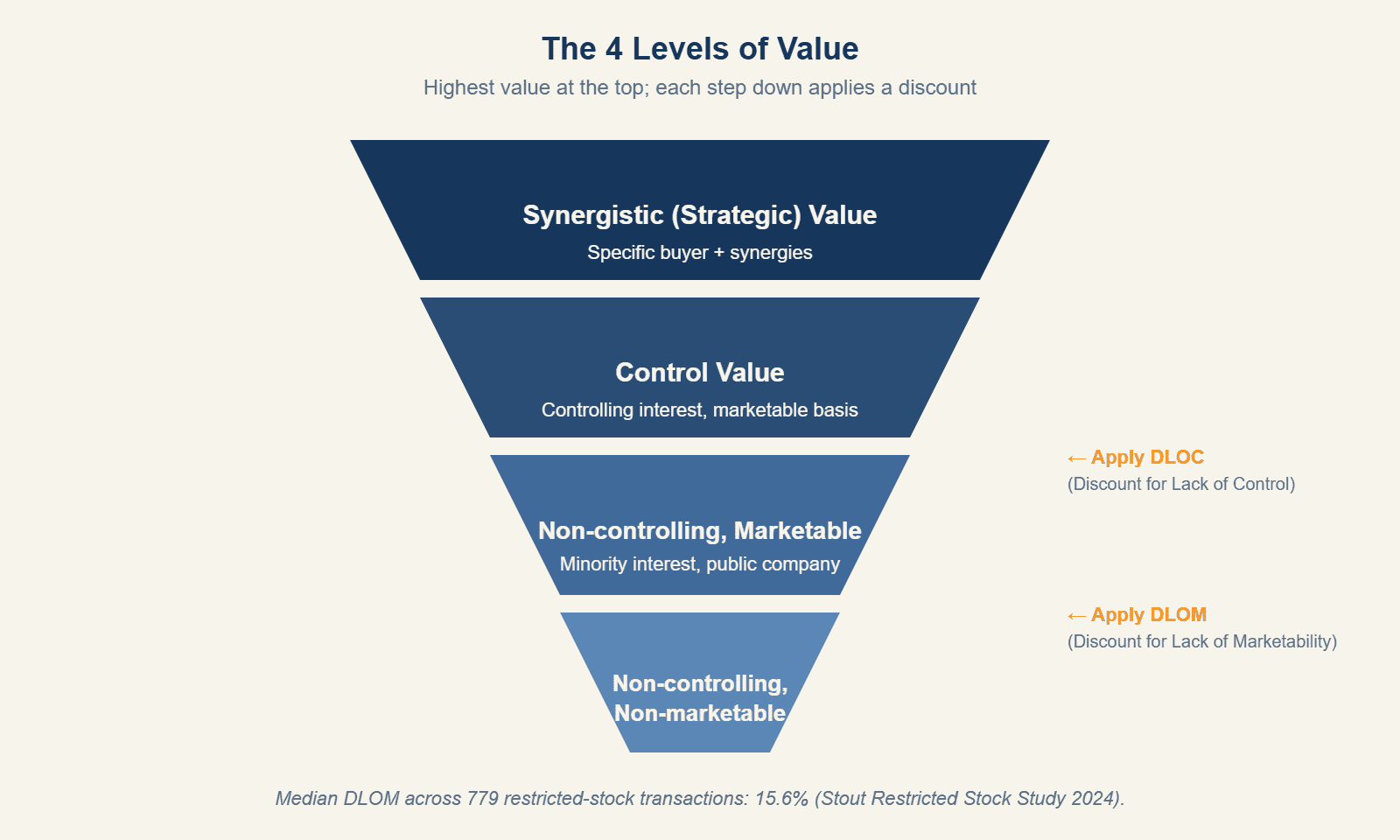

The five standards of value: which one applies to your situation?

The standard of value identifies the type of value being utilized in a specific engagement, and the wrong standard produces a defensible-but-wrong number. The International Glossary of Business Valuation Terms (adopted jointly by NACVA, AICPA, ASA, CICBV, and IBA in June 2001) defines five. The Pepperdine 2025 practitioner data shows that 76% of practitioners apply recast EBITDA multiples to whichever standard the engagement specifies, but the standard sets the lens, not the math.

- Fair Market Value (FMV). The price at which property would change hands between a hypothetical willing buyer and seller, neither under compulsion, both reasonably informed. The IRS standard. Revenue Ruling 59-60 lists eight aspects every FMV appraisal must consider. IRC Section 6662 penalizes misstatements. IRC Section 2703 limits how transfer restrictions can be used to depress FMV.

- Statutory Fair Value. Defined by state statute and case law. Often excludes the Discount for Lack of Control. Used in dissenting-shareholder, oppression, and partnership-dispute cases. Louisiana and Mississippi treat this differently than Delaware does. Know your jurisdiction.

- Financial Reporting Fair Value. Defined by ASC 820 as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.” Used in GAAP reporting, purchase price allocation, and goodwill impairment.

- Investment (Strategic) Value. The value to a specific buyer based on that buyer’s expectations and synergies. The “what would Buyer X pay” lens. Useful when an obvious strategic acquirer is in view.

- Intrinsic (Fundamental) Value. The value an analyst believes a business should be worth based on its fundamentals, independent of what the market is currently paying. Most often used in securities analysis.

A divorce valuation written under FMV when the state requires Fair Value is malpractice exposure. A gift-tax appraisal written under Investment Value will not survive IRS scrutiny. The standard is the first decision in the engagement, and it’s the one that should never be made casually.

Qualitative factors that actually move the multiple

The multiple a buyer pays isn’t a function of your industry code. It’s a function of risk-adjusted cash flow. Per the Stout Restricted Stock Study 2024, the median Discount for Lack of Marketability across 779 transactions was 15.6%, with a mean of 20.4%. That spread, almost five percentage points between median and mean, is the qualitative-factor story. Two businesses with identical EBITDA can carry very different multiples.

Eight factors show up in nearly every engagement we run. These are the levers that drive your number.

- Owner dependence. If the business can’t function for two weeks without you, the buyer is acquiring a job, not a company. Multiples compress accordingly.

- Customer concentration. When a single customer accounts for more than 15-20% of revenue, the discount stacks up. We’ve seen 1.5 turns of EBITDA come off a deal over concentration alone.

- Revenue predictability. Recurring revenue (contracts, subscriptions, repeat customers) commands a premium over project-based revenue. The premium widens as the recurring percentage rises.

- Gross margin trajectory. A flat or declining gross margin tells the buyer the business has lost pricing power. A rising gross margin tells the opposite story.

- Succession depth. Is there a credible #2 with a documented role and incentive to stay? If not, the key-person discount applies.

- Competitive moat. Defensible market position, switching costs, proprietary processes, regulatory licenses. The harder you are to displace, the higher the multiple.

- Financial cleanliness. Reviewed or audited financials, clear chart of accounts, defensible add-backs. Sloppy financials cost real dollars at the negotiating table.

- Industry trajectory. A rising tide raises every multiple in the sector. Headwinds compress them.

For minority-interest and tax-context engagements, the Mandelbaum framework (Mandelbaum v. Commissioner, T.C. Memo. 1995-255) provides the nine factors most courts use to support DLOM magnitude. We document each factor in the workpaper file because the alternative is a discount that gets argued down.

What buyers actually pay for goes deeper than these eight factors. The full owner-readiness framework (eight value drivers plus eight operational functions) is a separate post in this cluster. For this pillar, it’s enough to know that the multiple isn’t a market verdict on your industry. It’s a verdict on how you’ve built the business.

How does Duran Advisors value a business? The Facts-to-Conclusion five-step process

Every credentialed valuation we deliver follows the NACVA Facts-to-Conclusion framework: Preliminary, Pre-Hire, Engagement, Valuation, Report. Per the NACVA Professional Standards (June 2023 edition), the same five steps apply whether the engagement type is a Calculation or a Valuation, but the depth at each step shifts. Here’s what the work looks like end-to-end at Duran Advisors.

- Initial confidential consultation (30 minutes, no charge). We work through purpose, valuation date, intended users, standard of value, and the premise of value. This is where we establish whether you need a Calculation or a Conclusion, and we run a conflict check.

- Data request and recasting. We pull 3-5 years of tax returns, financial statements, AR/AP aging, customer lists, owner compensation history, and the off-balance-sheet items most owners forget to mention. Then we recast. Recasting financial statements is the unglamorous work where most amateur valuations break down. Reasonable compensation analysis, discretionary expense normalization, extraordinary item adjustments, and the operating-vs-non-operating split all happen here.

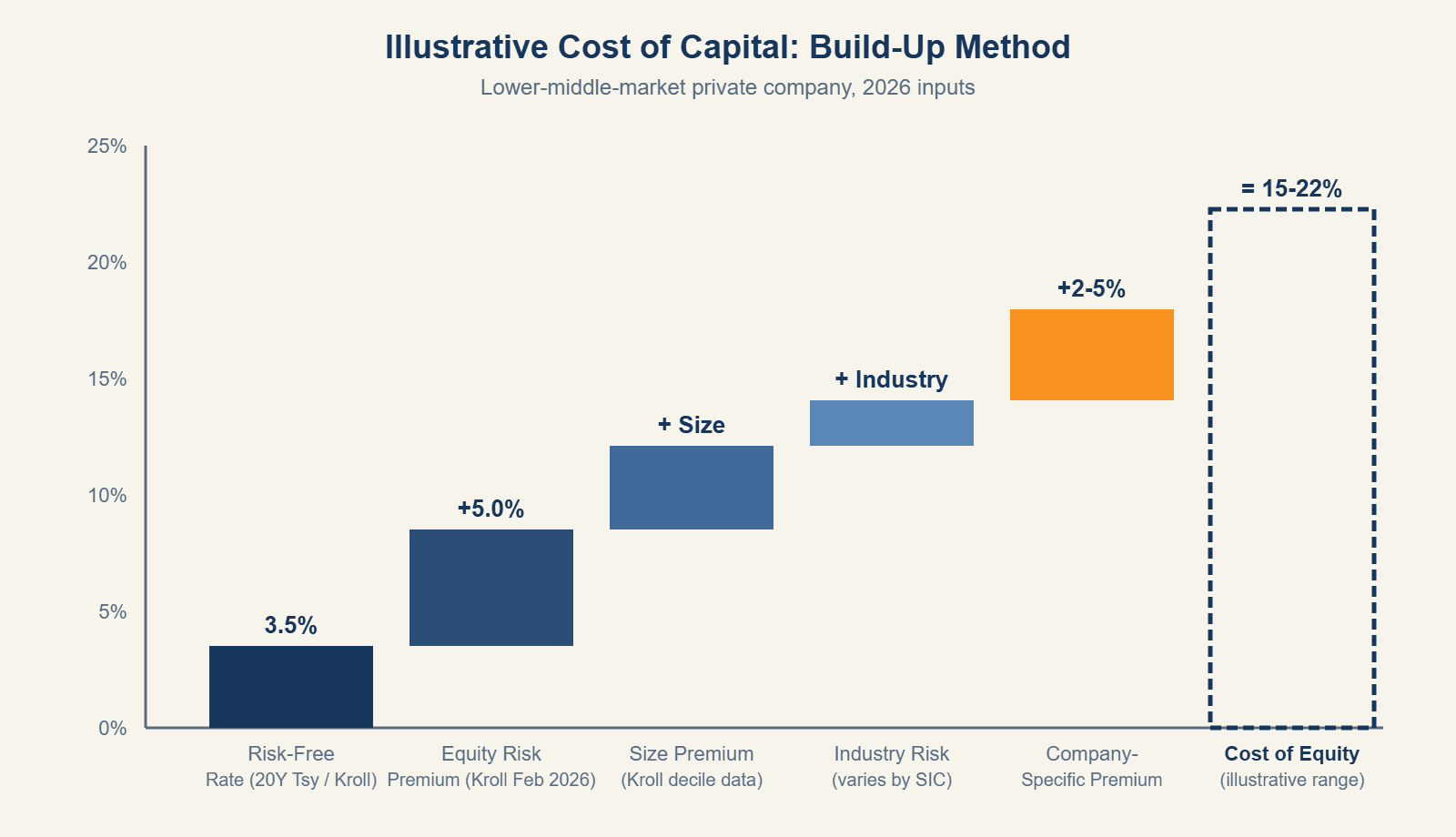

- Multi-approach analysis with market overlay. We apply all three approaches when an engagement supports it. For income, we typically use the Build-Up Method to derive the discount rate, anchored on Kroll’s reaffirmed 5.0% U.S. equity risk premium (February 2026) and the higher of Kroll’s 3.5% normalized risk-free rate or the spot 20-year Treasury yield. For market, we apply the 5/10/10 comp-selection rule to the transaction databases. For asset, we adjust the balance sheet to FMV. Then we reconcile.

- Coordinated review with your existing advisors. Your CPA reviews the recasting. Your attorney reviews the standard of value and any litigation context. Your financial planner reviews the estate or wealth-transfer implications. We bring them into the conversation early, not at the end, so the report serves the whole team.

- Final report and stress-test conversation. We walk you through the conclusion, the reconciliation, and the two or three places where a sharp opposing party would push back. You leave the meeting able to defend the number to a buyer, a lender, an examiner, or opposing counsel.

Turnaround at Duran Advisors:

Calculation of Value: 2-3 days standard, 24-hour rush available.

Conclusion of Value: 1-2 weeks standard, 72-hour rush available.Industry norm is roughly 5-10 times longer on Calculation and 3-4 times longer on Conclusion. This is the only window in which an owner can know exactly what the market thinks in under 30 days.

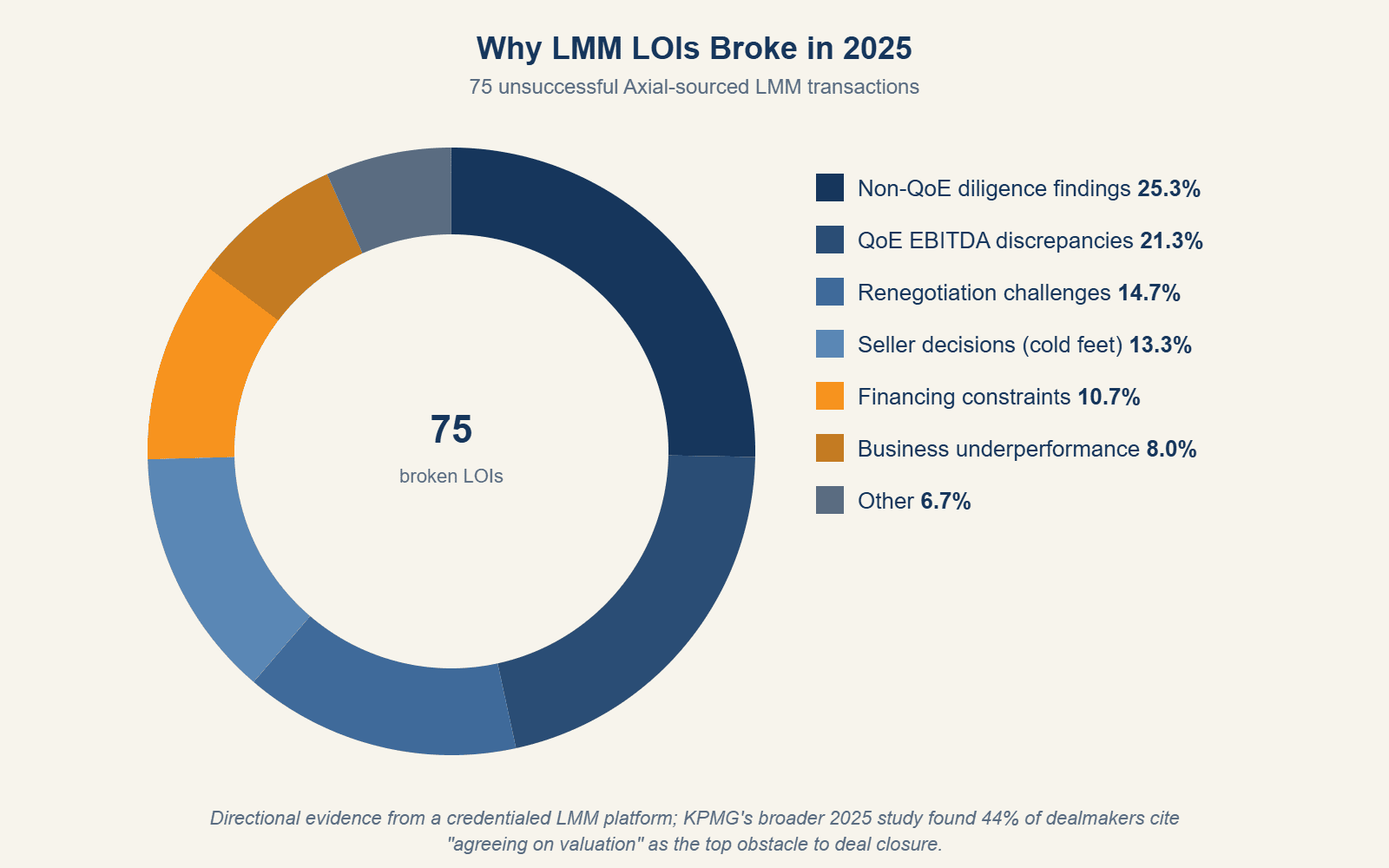

Why do deals fall apart at LOI? Where defensible valuation pays off

The valuation you commission before going to market determines how well your deal survives diligence. Per the Axial Dead Deal Report 2025, 25.3% of broken LOIs in 2025 traced to non-QoE diligence findings, and another 21.3% to QoE EBITDA discrepancies. Per the KPMG 2025 M&A Deal Market Study, 44% of dealmakers cite “agreeing on valuation” as the top obstacle to deal closure. Two different lenses, same conclusion.

What does this mean in practice? When the seller goes to market with a number that wasn’t stress-tested, the buyer’s diligence team finds the gap. The gap becomes a retrade. The retrade becomes a re-cut LOI or a dead deal. The LOI is not the close. It’s the start of a 90-day window in which everything you said about your business gets verified.

This is where Duran’s active sell-side practice shows up in the valuation work. We see what survives diligence and what doesn’t. The defensible add-back, the customer-concentration disclosure done early, the working-capital peg negotiated in the term sheet: each of these comes from running deals, not just modeling them. Per the IBBA Market Pulse Q4 2025 Survey, sellers averaged 76% to 89% cash at close across deal sizes. That number isn’t accidental. It’s what diligence-survivable valuations look like when they cross the finish line.

When to consult a valuation expert: two real engagements

Two patterns illustrate what active-practice valuation work actually looks like. Both anecdotes below are composite, anonymized to protect client identity, and reflect the kind of work we run every quarter for owners across South Louisiana and Mississippi.

A $500,000 enterprise value uplift

A multi-location restaurant group came to us before starting exit planning. The first step in our process is a business valuation and assessment. That assessment showed something the financials didn’t show: the business had real owner dependence.

We identified the most likely acquirer as a restaurant group and demonstrated that hiring a General Manager would add roughly $500,000 to enterprise value, net of the GM’s compensation. The owner agreed to hire the GM.

If we had not identified that opportunity on the front end, the owner would have left that money on the table. This is a common problem with for-sale-by-owner engagements. Sellers do not know what they do not know, so they make decisions that look right on the surface and still leave money on the table.

A $1.8 million appraisal correction

A buyer’s SBA-financed acquisition was stalled at the lender. The third-party valuation supporting the deal had used depreciated book value for the real estate. The business was an asset-heavy wholesale distribution company. Book value on the real estate was about $400,000. Fair market value of the same real estate, supported by a recent appraisal from a professional appraiser, was closer to $2.2 million. The mistake understated the value of the company by roughly $1.8 million, which left us about $1 million short of the appraised value the lender needed to clear SBA approval. The bank turned the deal down, saying it did not appraise.

I went through the appraisal line by line to recreate the numbers and realized the appraised value for the real estate had never been used. The lender then rejected the original valuation. The bank identified a new appraisal firm, the revised numbers came in where the deal needed them, and the transaction was approved for funding. Deals get lost like this all the time. Not having someone who truly understands how the numbers work is a huge liability when you are selling a business.

These aren’t edge cases. They’re what active-practice integration looks like when the valuation work is done by someone who also runs the sale.

How much does a business valuation cost?

Business valuation pricing varies with engagement type, deal size, and the level of defensibility required. Per the Federal Reserve’s April 2026 SLOOS, 8.9% of domestic banks tightened C&I lending standards for small firms in Q1 2026, which means the report quality required to clear SBA underwriting has risen. Cheap valuations don’t survive that scrutiny. The first conversation establishes scope, and the scope sets the fee.

- Calculation Engagement tier. Typically a four-figure engagement. Limited approaches, summary documentation, fast turnaround. Right when the use case is internal.

- Valuation Engagement (Conclusion of Value) tier. Higher fee. Multi-approach analysis, full reconciliation, complete workpaper file, defensibility against third-party challenge. Required for tax, SBA, litigation, ESOP, and most sale-support contexts.

- Rush premium. When the engagement compresses to a 24-hour Calculation or a 72-hour Conclusion, an analyst-time premium applies. The rush isn’t about cutting corners. It’s about clearing the analyst’s queue.

- Lowest-cost is rarely best. When a buyer’s diligence team finds a hole in a cheap report, the cost of correction shows up at the negotiating table. We’ve seen $200,000+ price adjustments traced to a weak initial appraisal.

- Free initial conversation. A 30-minute confidential call establishes whether you need a Calculation or a Conclusion, what the standard of value should be, and what the scope looks like. Schedule the conversation here.

How do you choose a valuation professional?

Choosing a valuation professional means weighing credentials and active transaction experience together. Per the BizBuySell Insight Report Q1 2026, 2,345 small businesses transacted in Q1 2026 at a median price of $350,000, but that headline blends Main Street with the lower-middle-market. Your valuation needs to be built for the kind of deal you actually have, by someone who has run that kind of deal recently.

Four standards bodies govern US business valuation practice. NACVA publishes Professional Standards (the latest publicly posted edition is June 2023). AICPA publishes SSVS-1, codified at VS Section 100, for CPAs performing valuations. ASA publishes the Business Valuation Standards (BVS-I through BVS-IX). The Appraisal Foundation publishes USPAP Standards 9 and 10. All four require independence, professional competence, sufficient relevant data, written engagement understandings, and appropriate documentation.

The market is full of valuation work done by people without credentials, without active transaction experience, or without both. A CPA who does two valuations a year is not the same as a credentialed valuator integrated into an active M&A practice. Ask the question directly: how many engagements does this practitioner run per year, what credentials back the work, and have they sat across the table from a buyer’s diligence team in the last 90 days?

Joel F. Duran founded Duran Advisors after 15+ years of M&A and business valuation work across the Gulf South. His active credentials are CM&AA (Certified Merger & Acquisition Advisor), M&AMI (Mergers & Acquisitions Master Intermediary), CM&AP (Certified M&A Professional), CEPA (Certified Exit Planning Advisor), CVGA (Certified Value Growth Advisor), Certified Value Builder™, CAIM (Certified Acquisition & Investment Manager), and CMSBB (Certified Main Street Business Broker). He is an IBBA Past Educator and an active member of M&A Source, AM&AA, IBBA, and the International Exit Planning Association. He is currently completing the NACVA Certified Valuation Analyst program; all Duran Advisors valuation engagements are performed under NACVA Professional Standards methodology.

The shorter version: we sell what we appraise. Active sell-side integration is the competitive moat. It’s the difference between a number on paper and a number that closes.

Frequently asked questions about business valuation

How long does a business valuation take?

At Duran Advisors, a Calculation of Value runs 2-3 days standard with a 24-hour rush available. A Conclusion of Value runs 1-2 weeks standard with a 72-hour rush. Per NACVA Professional Standards (June 2023), the industry norm runs 5-10 times longer on Calculation and 3-4 times longer on Conclusion. The speed differential is structural, built into our workflow rather than achieved by cutting analytical steps.

How accurate is a business valuation?

A defensible business valuation produces a range, not a single point. Per the Pepperdine 2025 Private Capital Markets Report, guideline transactions carry 33% method-weight on average, which means even credentialed work reconciles across multiple imperfect inputs. Accuracy improves with data quality, comp set discipline, and the integrity of the recasting. It compresses when the engagement skips steps.

Do I need a valuation if I’m not selling yet?

Yes, in most cases. Per the Exit Planning Institute 2025 Generational State of Owner Readiness, only 27% of owners have completed a formal valuation while 50%+ of Boomer owners plan to exit within five years. A baseline Calculation of Value sets the planning anchor for buy-sell funding, estate planning, value-driver work, and the eventual sale decision.

Will my CPA’s valuation hold up in court?

It depends on whether the CPA holds a valuation credential, performed a Valuation Engagement (not a Calculation), and worked under AICPA SSVS-1 documentation standards. Federal courts apply the Daubert framework to expert testimony. A tax-return-style opinion written by a CPA without valuation training is rarely sufficient for litigation. Get a Conclusion of Value from a credentialed valuator when court is in play.

What’s the difference between a Calculation and a Conclusion of Value?

A Calculation Engagement uses scope and methods agreed in advance with the client and produces a Calculated Value. A Valuation Engagement uses the valuator’s full professional judgment across all relevant approaches and produces a Conclusion of Value. Per NACVA Professional Standards, the Conclusion of Value carries the documentation and defensibility required for IRS, SBA, court, and ESOP contexts.

Can I value my business myself?

For an internal directional read, sure. For any context with an external counterparty (buyer, IRS, court, lender, partner), no. Per the KPMG 2025 M&A Deal Market Study, 44% of dealmakers cite valuation disagreement as the top obstacle to deal closure. Self-valuations rarely survive an opposing party’s diligence, and the cost of correction usually exceeds the cost of doing it right the first time.

What documents do I need to provide?

The standard package: 3-5 years of tax returns and financial statements, year-to-date interim financials, AR/AP aging, fixed-asset schedule, owner compensation history, customer concentration data, real estate and equipment lease detail, and any shareholder or operating agreements. Litigation, estate, and SBA contexts add jurisdiction-specific items. The data request goes out within 24 hours of engagement.

How are buy-sell agreements typically valued?

Three structures dominate: fixed-price (updated annually), formula-based (multiple of book value or earnings), and independent appraisal at trigger. Formula clauses tend to age badly because the formula stops matching the market. Independent valuation at trigger, with the methodology specified in the agreement, is the most defensible structure. The valuation funding must match the insurance funding or the agreement collapses on first claim.

What if I disagree with the valuation?

Good valuators expect pushback and document their reasoning so a sharp third party can audit the work. If you disagree, the right next step is a stress-test conversation: walk through the assumptions, the comp set, the discount rate build-up, and the reconciliation weighting. Disagreements usually resolve into a refined data point or a documented difference of professional judgment. Either outcome is defensible.

Is a business valuation tax-deductible?

In most cases, yes, when the valuation is performed for a business purpose (estate planning, financing, sale preparation, buy-sell funding, partnership disputes). Personal-use valuations (divorce, for example) follow different rules. Confirm the specific deduction treatment with your CPA, since the answer depends on whether the engagement supports an ordinary business expense, a capital transaction, or a tax-position substantiation.

Ready to know what your business is actually worth?

A defensible business valuation isn’t an expense. It’s the input that makes every other decision better: when to sell, how to fund a buy-sell, what to put on a balance sheet for estate planning, where to invest the next dollar of value-driver work. The owners who treat valuation as planning infrastructure tend to exit on their own terms. The ones who wait until the buyer is at the table tend to renegotiate.

Duran Advisors serves business owners in New Orleans, the North Shore, Metairie, Baton Rouge, Houma-Thibodaux, and South Mississippi. Our practice combines active sell-side M&A with credentialed valuation work performed under NACVA Professional Standards methodology. We sell what we appraise. The 30-minute initial conversation is confidential and at no charge. Learn more about our valuation services here.