A letter of intent (LOI) in a business sale is a mostly non-binding term sheet that, once signed, fixes the headline economics of your deal: the purchase price, the deal structure, working-capital expectations, and a binding exclusivity period that lets the buyer begin formal due diligence. In M&A, the LOI is the hinge between negotiation and closing, and the terms you accept here shape every conversation that follows.

By Joel F. Duran, Principal Advisor at Duran Advisors. CM&AA, M&AMI, CM&AP, CEPA, CVGA, Certified Value Builder™, CAIM, CMSBB; IBBA Past Educator; active member of M&A Source, AM&AA, IBBA, and the International Exit Planning Association. 15+ years of M&A and business valuation experience across the Gulf South. Last updated: June 6, 2026.

Key takeaways

- An LOI sets price, deal structure, and an exclusivity window before the binding purchase agreement is ever drafted.

- Most of an LOI is non-binding, but exclusivity, confidentiality, and expense clauses usually are. Know the difference before you sign.

- The biggest seller risks hide in the fine print: an open-ended no-shop, a vague working-capital peg, and room for the buyer to re-trade the price during diligence.

- A competitive process and clean, diligence-ready books are your strongest protection against a post-LOI price cut.

What a Letter of Intent Actually Does

An LOI documents a meeting of the minds on the major terms before attorneys draft the definitive purchase agreement. It usually arrives after a buyer has reviewed your confidential information memorandum, met your management team, and submitted an indication of interest. Signing it moves the deal from courtship to commitment, and it tells both sides the relationship is serious enough to spend real money on lawyers, accountants, and diligence.

In a typical sale process, the LOI is roughly the fourth milestone: prepare the business, take it to market, field offers, then sign an LOI with the buyer you choose. If you have not already done the groundwork, read how to prepare your business for sale first, because the strength of your preparation is exactly what determines how favorable your LOI terms can be.

What’s Inside an LOI: The Terms Sellers Must Read Closely

An LOI is short, often three to six pages, but each term carries weight. The document sketches the deal that the definitive agreement will later formalize, so the language you accept now becomes the starting line for every negotiation to come. These are the provisions that matter most to a seller.

Purchase price and how it is expressed

Price is rarely a single flat number. It is usually expressed as an enterprise value, often a multiple of EBITDA, on a cash-free, debt-free basis. The headline figure means little until you know how EBITDA is defined and which add-backs the buyer accepts. A defensible business valuation is what lets you push back when a buyer’s number is built on a thinner version of your earnings than reality supports.

Deal structure: how you actually get paid

Two LOIs with the same price can deliver very different outcomes. Structure determines how much you receive at close versus over time: cash at closing, a seller note, an earnout tied to future performance, or rollover equity in the new company. Earnouts in particular shift risk onto the seller. According to SRS Acquiom’s 2025 M&A Deal Terms Study, summarized by the Harvard Law School Forum on Corporate Governance, earnouts appeared in roughly 22% of private deals in 2024, and the median earnout equaled about 31% of the closing payment. The American Bar Association’s 2023 Private Target M&A Deal Points Study, reviewed by K&L Gates, found earnouts in 26% of reported deals (for transactions between $30 million and $750 million). In practice, a meaningful slice of your “price” can be contingent, so read the structure as carefully as you read the number.

The working-capital peg

This is the term most owners overlook and most regret. The buyer expects to receive a “normal” level of working capital with the business, set by a target, or peg. If your working capital at close falls below the peg, your proceeds get reduced dollar for dollar. A vague or buyer-friendly peg can quietly erase six figures from your check. Insist the LOI describe how the peg will be calculated, not just promise to settle it later.

Exclusivity, diligence, and your post-close role

The LOI also sets the exclusivity (no-shop) period, the scope and timeline of due diligence, the conditions that must be met to close, and what happens to you and your key employees afterward. Each of these is negotiable. An open-ended exclusivity period or an unlimited diligence demand hands the buyer leverage you will wish you had kept.

A quick example: why structure beats the headline number

Picture two buyers who both “offer $6 million.” Buyer A pays $6 million in cash at close. Buyer B pays $4 million at close, $1 million in a five-year seller note, and a $1 million earnout tied to next year’s results. On paper the offers match. In reality, Buyer A hands you certainty, while a third of Buyer B’s price depends on future performance and the note being repaid. When we evaluate LOIs at Duran Advisors, we model each structure’s actual cash to you, after the working-capital peg, before deciding which “equal” offer is really the stronger deal. The headline number is where the conversation starts, not where it ends.

Is an LOI Binding? Binding vs. Non-Binding Provisions

Most of an LOI is non-binding: price and structure are stated intentions, not enforceable promises, until the definitive purchase agreement is signed. But specific clauses are almost always binding the moment you sign, and sellers routinely miss them. Knowing which is which is the single most important thing to understand before you put your name on the page.

| Usually non-binding | Usually binding |

|---|---|

| Purchase price and valuation | Exclusivity / no-shop |

| Deal structure (note, earnout, rollover) | Confidentiality |

| Working-capital target | Expense allocation / break costs |

| Conditions to closing | Governing law and dispute terms |

The takeaway: the parts that protect the buyer tend to be binding, and the parts that protect your economics tend not to be. That asymmetry is exactly why the negotiation of an LOI matters, and why so much of a seller’s leverage is spent or preserved at this stage.

Seller Protections to Negotiate Before You Sign

Once you sign, your negotiating power drops, because you have agreed to stop talking to other buyers. The protections below are far easier to secure in the LOI than to claw back later. Negotiate them while you still have a competitive process behind you.

- Cap the exclusivity window. Push for 30 to 60 days, with any extension tied to the buyer making documented progress. Open-ended no-shops are a red flag. Law firm Goodwin’s M&A deal database found the share of deals with exclusivity periods of 61 days or longer jumped from roughly 6% in 2021 to nearly 40% in 2022, so the pressure to grant long windows is real. Hold the line.

- Pin the price to specifics. Define EBITDA, list the accepted add-backs, and state the multiple. The more precise the price language, the less room a buyer has to “reinterpret” it during diligence.

- Define the working-capital peg now. Spell out the calculation method and the reference period in the LOI, not in a side conversation three weeks before close.

- Bound the diligence period and information demands. Agree on a diligence timeline and a reasonable scope so the process does not drift indefinitely.

- Address expenses and good faith. Clarify who bears costs if the deal collapses, and ensure both sides commit to negotiating the definitive agreement in good faith.

What Is a Re-Trade, and How to Limit It

A re-trade is when a buyer lowers the price or worsens the terms after the LOI is signed, usually citing something uncovered in due diligence. Because you have agreed to stop talking to other buyers during exclusivity, a late re-trade puts you in a weak position: walk away and restart the entire process, or accept less than you agreed. The defense against a re-trade starts long before the LOI is on the table.

The single best protection is a competitive process. When a buyer knows other credible bidders exist, the cost of an opportunistic re-trade goes up, because you have a real alternative. Clean, diligence-ready financials are the second line of defense; surprises are what give a buyer the excuse to renegotiate, and a recasting that has already been stress-tested leaves little to “discover.” Tight LOI language is the third: the more precisely price and structure are defined, the harder it is to reopen them.

This is also why the speed and structure of the sale process matter. At Duran Advisors, our Structured Sale™ process is built so that you will know what the market actually thinks of your business in under 30 days, before exclusivity ever narrows your options. A short, competitive window leaves a buyer far less room to grind you down after the LOI than a slow, single-buyer negotiation does.

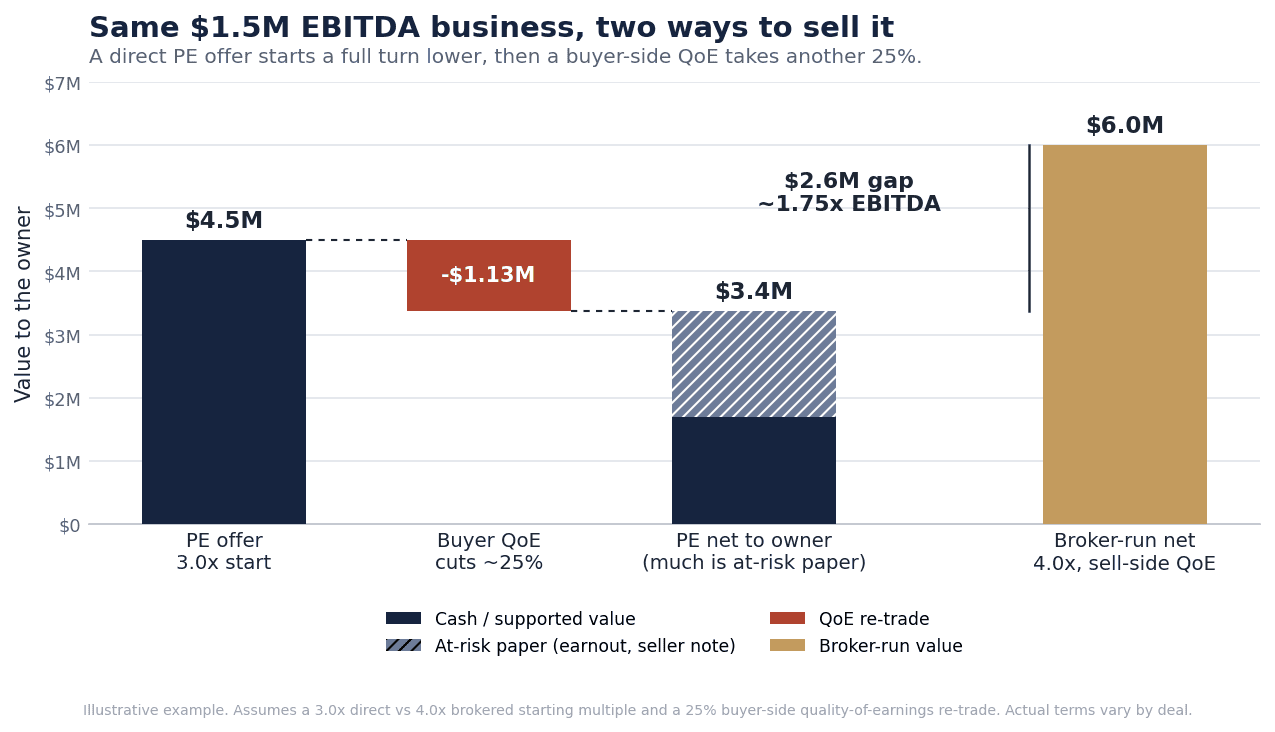

The pattern we see most often: the direct private-equity approach

Here is the version of this that crosses our desk most often. A private equity group contacts an owner directly, friendly and complimentary, and moves quickly to get a non-binding LOI signed. Because it is non-binding, almost none of the terms are actually locked. Once the owner is inside exclusivity and no longer talking to anyone else, the grind starts: a deduction here, a revised assumption there, a working-capital adjustment, a slice of the price shifted into an earnout. The owner has become a captive audience, and the final number drifts well below where it began.

About one in five calls we receive comes from a CPA, attorney, or financial planner whose client is sitting in exactly this position. In the deals we see, the price these owners get walked down to lands roughly a full turn of EBITDA below what a competitive process would have produced. On a business doing a few million dollars in EBITDA, that is not a rounding error. It is a life-changing amount of money.

What makes the gap so wide is not only the opening number. It is what happens during due diligence. A buyer-side quality of earnings (QoE) report, the deep review of your financials a buyer commissions, is routinely used by direct acquirers to justify shaving the price further, often by a quarter or more. In a competitive, broker-run process, we bring our own sell-side QoE to the table, so the number is already defended before a buyer can chip it. Here is how the same $1.5 million EBITDA business can play out two ways.

| Deal term | Direct PE offer (owner alone) | Broker-run Structured Sale |

|---|---|---|

| Starting multiple | 3.0x (a full turn lower) | 4.0x |

| Starting enterprise value | $4.5M | $6.0M |

| Quality of earnings outcome | Buyer’s QoE used to cut value ~25% | Sell-side QoE supports the full price |

| Value after QoE | $3.4M | $6.0M (holds) |

| Cash at close | ~50% (about $1.7M) | ~85 to 90% (about $5.3M) |

| Seller note (you finance the buyer) | Large, long, below-market | Minimal or none |

| Earnout (buyer-controlled, long tie-down) | Large, multi-year | None, or small and achievable |

| Rollover equity | Illiquid minority stake | Optional, with protections |

| Working-capital peg | Vague, clawed back at close | Defined formula, no surprise |

| Indemnity escrow / holdback | 20% for 24 months | 5% for 12 months, plus R&W insurance |

| Non-compete and employment | 5-year non-compete, 3-year forced employment | Reasonable scope, market-rate transition |

| Likely value the owner nets | ≈ $3.4M (~2.3x), much of it at-risk paper | ≈ $6.0M (4.0x) |

The fix is almost always the same. Before you sign, or before the grind goes any further, have someone run a confidential, competitive process so the market sets your number instead of a single buyer. If an unsolicited offer is on your desk right now, schedule a confidential conversation with us before you respond.

How an M&A Advisor Protects You at the LOI Stage

An experienced M&A advisor runs a competitive process, stress-tests every term in the LOI against current market norms, models how each structure actually pays you out against an independent business valuation, and coordinates with your CPA and attorney so nothing falls through the cracks. The LOI is where deal-saving leverage is either spent or preserved, and it is far easier to negotiate well with a specialist who has read hundreds of these documents than to learn on your own deal.

A real example: an unsolicited offer that was not what it looked like

A while back, a CPA called us about a client who had received an unsolicited offer for his commercial marine business, which was doing about $14 million in sales and around $3 million a year in EBITDA. The owner was excited. A family office wanted in, and the headline sounded like a win.

The details told a different story. Once we worked through the structure, the owner would have sold 80% of his company and, after the business’s debt was paid off, walked away with about $1 million in cash. The family office would have owned the majority of a business whose hard assets alone were worth more than they were paying. If the company ever failed, its liquidation value would have more than repaid them. They were taking almost no risk, and the owner was handing over control of a $3 million EBITDA business for a fraction of its value.

There was also a large revenue stream the business was outsourcing entirely. On top of its roughly $14 million in sales, about $25 million a year in rentals was flowing to third parties, close to $39 million in total activity moving through the operation. With the right investment, much of that $25 million could have been pulled in-house. The upside the owner was about to give away was enormous.

He did not sign. Our advice was to keep control and run a value acceleration program to capture that upside first, then sell from a position of strength. That is the difference between reading an offer and understanding one.

Duran Advisors serves owners of businesses with roughly $1 million to $25 million in revenue across New Orleans, the North Shore, Metairie, Baton Rouge, Houma-Thibodaux, and South Mississippi. Our approach rests on three things owners tell us they value most: deep regional market expertise, a coordinated advisor team that works alongside your existing CPA and attorney, and an education-driven process so you understand every term you are agreeing to. You stay in control of the decision; we make sure you are making it with full information.

Frequently Asked Questions

Is a letter of intent legally binding?

Mostly no. The price, structure, and other commercial terms in an LOI are non-binding until the definitive purchase agreement is signed. However, certain clauses, typically exclusivity, confidentiality, and expense allocation, are binding the moment you sign. Always read the LOI to confirm which provisions are enforceable before you agree.

How long is the exclusivity period in an LOI?

In lower-middle-market deals, exclusivity commonly runs 30 to 90 days, and buyers increasingly push for longer windows. Sellers should aim for 30 to 60 days, with extensions granted only if the buyer is making documented progress. An open-ended no-shop removes your leverage and should be resisted.

Can a seller negotiate an LOI?

Yes, and you should. The LOI is the point of maximum seller leverage, before exclusivity limits your options. Price language, deal structure, the working-capital peg, the exclusivity window, and the diligence timeline are all negotiable. Terms accepted in the LOI are very hard to improve later, so negotiate hard upfront.

What happens after the LOI is signed?

The buyer begins formal due diligence, examining your financials, contracts, operations, and legal standing, while attorneys draft the definitive purchase agreement. This phase typically takes several months. You continue running the business, respond to diligence requests, and negotiate final terms toward closing, all within the exclusivity period you agreed to.

Can a buyer back out after signing an LOI?

Generally yes, because the commercial terms are non-binding. A buyer can walk away or attempt to renegotiate based on diligence findings, which is known as a re-trade. This is precisely why a competitive process, clean financials, and precise LOI language matter; they raise the cost of walking away or cutting the price.

Should I accept the first LOI I receive?

Not automatically. The first LOI sets your baseline, but the highest headline price is not always the best deal once structure, earnouts, and the working-capital peg are weighed. Comparing multiple offers, ideally from a competitive process, is how you learn what your business is truly worth to the market.

Thinking about selling, or looking at an LOI on your desk right now? Before you sign anything, schedule a confidential conversation with Duran Advisors. We will walk you through the terms, model what the deal actually pays you, and make sure you sign from a position of strength.